Land tax has become one of the most underestimated forces shaping long term property investment outcomes in Australia. Not because it is new, but because its interaction with ownership structure, aggregation rules, and trust treatment compounds quietly over time.

For many investors, land tax is treated as an annual expense to be minimised. For sophisticated investors, it is recognised as a structural consequence of how assets are held. That distinction matters.

The real risk is not land tax itself. The real risk is discovering too late that the structure supporting your portfolio cannot scale without triggering stamp duty, capital gains tax, or material lending friction.

This article examines land tax in Victoria and New South Wales in 2026, but more importantly, it explains why experienced investors frequently accept higher land tax outcomes in exchange for long term control, flexibility, and portfolio resilience through a family trust with a corporate trustee.

It also includes a practical appendix based on a state-by-state discussion (personal name vs trust / corporate trustee), showing how land tax behaves across Australia once timing, aggregation, and portfolio scale collide.

Land tax is not the enemy. Poor structure is.

Early stage investors often ask a single question: how do I pay the least tax this year?

That mindset works when portfolios are small. It becomes increasingly fragile as asset count, land value, and borrowing exposure grow.

Land tax is not merely an annual cost. It is the outcome of aggregation. It reflects how assets are grouped, how thresholds apply, and how decisions made early compound over decades.

The true danger is not paying land tax. The danger is building a portfolio that cannot adapt once scale introduces complexity.

How Victoria and New South Wales behave as portfolios scale

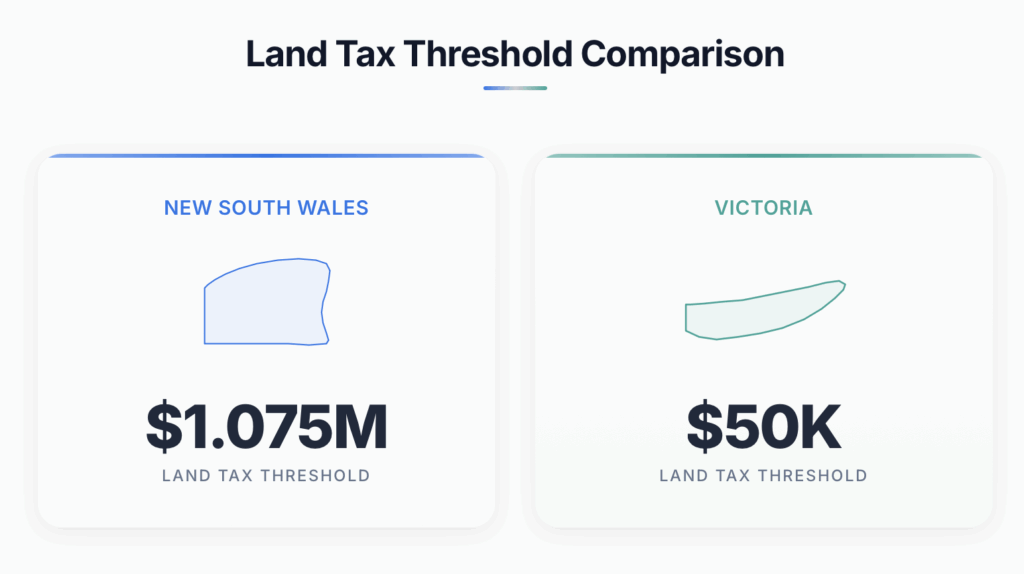

Victoria and New South Wales apply fundamentally different land tax frameworks once trusts enter the picture, and those differences only become meaningful at scale.

In Victoria, family trusts are generally assessed from the first dollar of land value at trust surcharge rates, with no tax free threshold. This increases annual land tax but provides structural separation between assets.

In New South Wales, individuals benefit from a general land tax threshold. Most family trusts are treated as special trusts and taxed at flat rates without a threshold. Fixed trusts, when structured and recognised correctly, can access more favourable treatment.

Viewed narrowly, this makes trusts appear inefficient. Viewed strategically, it highlights why experienced investors look beyond headline tax outcomes.

Why experienced investors still use family trusts

A family trust with a corporate trustee is almost never selected because it produces the lowest land tax bill in the early years.

It is selected because it solves problems that only emerge once portfolios become meaningful in size.

Those problems include risk concentration, loss of asset control, lending constraints, succession complexity, and the inability to restructure without triggering significant tax events.

The corporate trustee provides clean legal control without personal exposure. The family trust allows income and control to be adjusted as circumstances evolve. Together, they create a structure designed to hold assets for decades, not transactions.

Yes, this approach can result in higher land tax in some states. Experienced investors accept this trade off because alternative structures often fail first.

Land tax comparison up to $1,000,000 of land value

The table below illustrates how land tax outcomes behave across common ownership structures as land value increases. It is designed to show directional behaviour rather than provide personalised advice.

| Land value | VIC fixed trust | VIC personal | VIC family trust | NSW personal | NSW family trust | NSW fixed trust |

|---|---|---|---|---|---|---|

| $250,000 | $975 | $975 | $1,901 | $0 | $4,000 | $0 |

| $500,000 | $1,950 | $1,950 | $3,588 | $0 | $8,000 | $0 |

| $750,000 | $3,150 | $3,150 | $5,725 | $0 | $12,000 | $0 |

| $1,000,000 | $4,650 | $4,650 | $8,163 | $0 | $16,000 | $0 |

Important clarification. These figures are based on land value, not property value. Land value represents the unimproved value of the land only and excludes buildings or renovations.

How lending changes the equation

Land tax should never be assessed in isolation. For investors pursuing scale, borrowing capacity often becomes the binding constraint.

When a positively geared property is held within a trust, many lenders assess income and liabilities at the trust level. In practice, this can reduce the drag on personal serviceability and allow portfolios to continue expanding.

This is why sophisticated investors evaluate tax outcomes, lending policy, and structure as a single system rather than separate decisions.

Who this strategy actually suits

A family trust with a corporate trustee is not a default structure. It is a deliberate strategic choice.

It is most appropriate for investors who:

• Are building a large, diversified portfolio

• Intend to invest across multiple states

• Prioritise long term control over short term optimisation

• Aim to replace employment income with asset based cash flow

For these investors, higher land tax in certain years is often an accepted cost rather than a failure of planning.

Final perspective

Successful property investment is not about winning every tax line item. It is about building a portfolio that can grow, adapt, withstand policy changes, and deliver long term outcomes.

Experienced investors plan structure first, accept trade offs consciously, and optimise for scalability rather than short term savings. Land tax is part of that equation, not the headline.

To explore more data driven insights, visit our blog or learn how we support investors through our services.

Appendix — State-by-state trust vs personal outcomes

Land tax comparison by state

| State / Territory | Personal name threshold (unimproved land value) | Trust / corporate trustee threshold (as stated) | $1,000,000 land value land tax (Personal) | $1,000,000 land value land tax (Trust / corporate trustee) | Key call-outs mentioned |

|---|---|---|---|---|---|

| WA | $300,000 | Same as individual ($300,000) | ~$2,730 | ~$2,730 | Same cost personal vs trust; mentions “Metropolitan Regional Improvement Tax”; can “kick the can” with separate trusts to reuse threshold |

| NT | $0 | $0 | $0 | $0 | No land tax |

| QLD | $600,000 | $350,000 | ~$4,500 | ~$12,500 | Large gap personal vs trust; threshold not indexed for a long time (as said); primary production exemption discussed (must be genuine/feasible) |

| NSW | $1,075,000 | Trust treated with no threshold (as said) | $0 (at $1m land value) | $16,000 | NSW threshold “capped” ; unit trust note depends on unit holder; company (Pty Ltd) gets individual-like threshold in NSW (with CGT / “tax at the tail” trade-offs) |

| ACT | No threshold (fixed base + AUV model) | Same as personal | ~$12,293 (=$1,693 + $10,600) | ~$12,293 | Investor-only annual charge structure described; 1 July 2024 changes mentioned; conveyance duty noted separately |

| VIC | $50,000 | $25,000 | $4,650 | $8,163 | Trust cost ~close to double personal; windfall gains tax mentioned separately |

| TAS | Assumed $125,000 (as discussed) | Assumed same ($125,000) | $9,238 | $9,238 | Wording ambiguous but treats trust assessed like individual; same cost at $1m |

| SA | $833,000 (as stated for 25–26) | $25,000 | $1,340 | $6,340 | Very favourable in personal name; trusts get almost no threshold |

Best approach by state

WA

✅ Personal vs trust cost is the same at $1m land value (~$2,730), so structure choice is less about land tax and more about strategy (asset protection, distributions, lending).

✅ Mentioned tactic: multiple trusts/entities can “kick the can” and reuse thresholds (if planned properly).

✅ If it may become your home, they indicated keeping it in your own name for residence-related benefits.

NT

✅ Land tax is $0 regardless of structure, so structure choice is not driven by land tax here.

✅ Framed as a simpler holding-cost environment for investors.

QLD

✅ Personal name is materially cheaper than trust at $1m land value (~$4,500 vs ~$12,500).

✅ If using trusts, they stressed being switched on (entity/trustee choices and land value planning).

✅ Primary production exemption discussed, but they stressed it must be a genuine, feasible, profit-seeking enterprise.

NSW

✅ For the $1m land value example used: personal name was $0, trust was $16,000 (no threshold for trust as described).

✅ They highlighted a third lever: a Pty Ltd company gets an individual-like threshold in NSW (as stated), but warned about CGT discount loss and “tax at the tail” mechanics when extracting profits.

✅ Core message: don’t default to trust without modelling the holding cost impact.

ACT

✅ Same annual charge model regardless of personal vs trust (fixed base + AUV structure described).

✅ At $1m land value, they quoted ~$12,293 annually (=$1,693 + $10,600).

✅ Structure doesn’t change the annual bill in their description, so you plan around the ongoing cost.

VIC

✅ Trust is materially higher at $1m land value ($4,650 personal vs $8,163 trust).

✅ They framed it as a deliberate trade-off: the additional holding cost must be justified by strategy and plan.

TAS

✅ In their discussion, trust and personal were treated the same at $1m land value ($9,238).

✅ Land tax doesn’t drive structure choice much in their example, but the absolute cost is still meaningful.

SA

✅ SA was presented as very favourable in personal name at $1m land value ($1,340) due to the high threshold.

✅ Trust threshold was said to be $25k, making trust ownership much harsher ($6,340 at $1m).

✅ Their stated approach: absorb personal thresholds, then consider structure later.

If you flip it: best states by approach (from the same $1m example)

Best states if buying in your personal name (using their $1m example)

• NT: $0

• NSW: $0 (at $1m land value example discussed)

• SA: $1,340

• WA: ~$2,730

• VIC: $4,650

• QLD: ~$4,500

• TAS: $9,238

• ACT: ~$12,293

Best states if buying in a trust / corporate trustee (using their $1m example)

• NT: $0

• WA: ~$2,730

• SA: $6,340

• VIC: $8,163

• TAS: $9,238

• ACT: ~$12,293

• QLD: ~$12,500

• NSW: $16,000

Biggest “trust penalty” environments (trust materially worse than personal, per their numbers)

• NSW: $0 vs $16,000

• QLD: ~$4,500 vs ~$12,500

• VIC: $4,650 vs $8,163

• SA: $1,340 vs $6,340

Extra takeaways embedded in the conversation

✅ Their main warning is not “trust bad”, it’s “trust too early can wreck you” — especially once holding costs start compounding and you lose flexibility to restructure without major tax friction.

✅ They frame land tax as an “unproductive cost” that can quietly strip portfolio performance over time, even when portfolios look “successful” on paper.

✅ They repeatedly translate land tax into a weekly rent haircut to make the cash flow reality obvious.

✅ They point out state differences in timing/assessment (for example, when bills land) as a cash flow planning issue, not just a tax issue.

✅ NSW nuance discussed: company threshold in NSW (as stated) can reduce land tax versus trust, but introduces CGT and extraction trade-offs (“tax at the tail”).

✅ Queensland nuance discussed: primary production concessions exist but are policed and require genuine feasibility — not token activity.